There’s a tendency right now to look at the housing market and assume something has broken.

Sales are slower. Buyers hesitate. Deals fall apart that would have sailed through two years ago. And the easy conclusion—the one you’ll hear repeated—is that demand just isn’t there.

But that’s not what the data says.

What it says—clearly, and across multiple sources—is something more uncomfortable:

The demand is still there. The math just doesn’t work anymore.

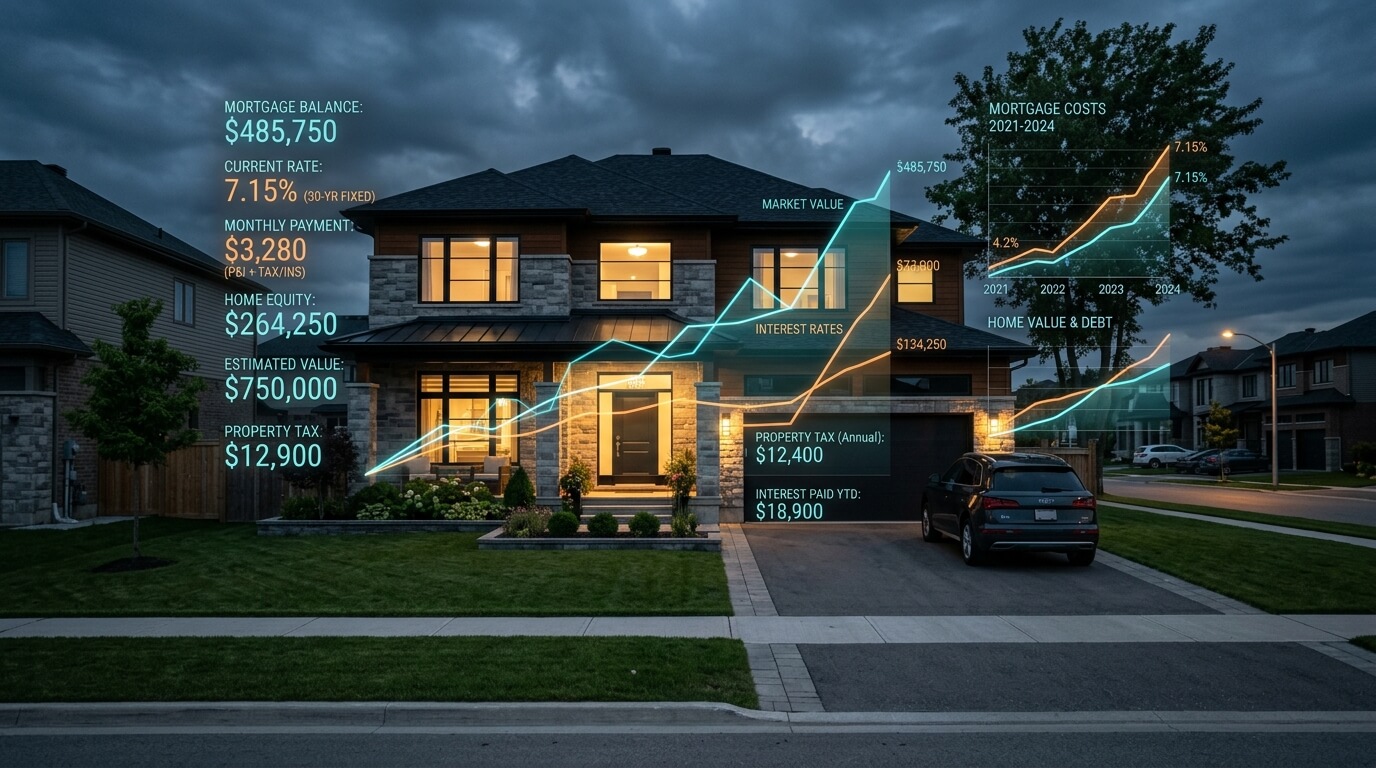

According to ATTOM’s latest Q1 2026 Home Affordability Report, homes are less affordable than historical norms in 97% of U.S. counties, and in nearly 70% of those markets, the typical buyer would have to spend more than the standard threshold of their income just to make the numbers pencil.

That’s not a cyclical slowdown. That’s a structural constraint. And once you see it that way, a lot of what’s happening in the market starts to make more sense.

You can see it in how construction is behaving.

Private residential construction spending slipped again to start the year, with single-family activity now down meaningfully year-over-year (2.3% higher a year ago), according to U.S. Census data and NAHB analysis. Builders aren’t pulling back because they’ve lost confidence in housing long-term—they’re adjusting to a buyer who is far more fragile than the headlines suggest.

You can see it in where people are moving.

New Census data, analyzed by The Wall Street Journal, shows a continued shift toward more affordable regions. Midwestern cities like Columbus and Lansing are gaining residents, while high-cost coastal markets are stabilizing rather than surging.

That’s not just a lifestyle preference—it’s an effort to make hard-earned dollars go further.

And you can see it in how buyers behave at the margin.

When affordability is stretched this far, it doesn’t take much—a small move in rates, a rise in insurance, a delay in closing—to push a deal from “yes” to “not right now.” The buyer doesn’t disappear, but steps back.

This is the part of the cycle that gets misunderstood because demand appears to be weakening on the surface. But underneath, what’s really happening is that demand is being filtered by affordability, by monthly payment, by the simple reality of what a household can carry.

The housing market isn’t short on interest. It isn’t short on need. It isn’t even short on buyers, in the abstract.

It’s short on affordability, which works in the real world.

And until that changes, the advantage won’t go to the builders who wait for conditions to improve. It will go to those who can operate cleanly, move efficiently, and close within the narrow window the market is still allowing.

Want to see how some builders are still growing—even as affordability tightens?

They’re not relying on the market to fix itself.

They’ve changed how they structure their deals, how they deploy capital, and how they move projects through the pipeline—so they can close inside the narrow window the market still allows.

We break that down step by step in Built to Prosper—and right now, we’re sending copies to qualified spec home builders.