The latest from HousingWire confirms something we’ve been pointing to for months: this isn’t a collapse—it’s a misalignment.

Over the past decade, housing cycles haven’t turned on price alone. They turn when seller expectations and buyer behavior drift apart. That’s exactly where we are now.

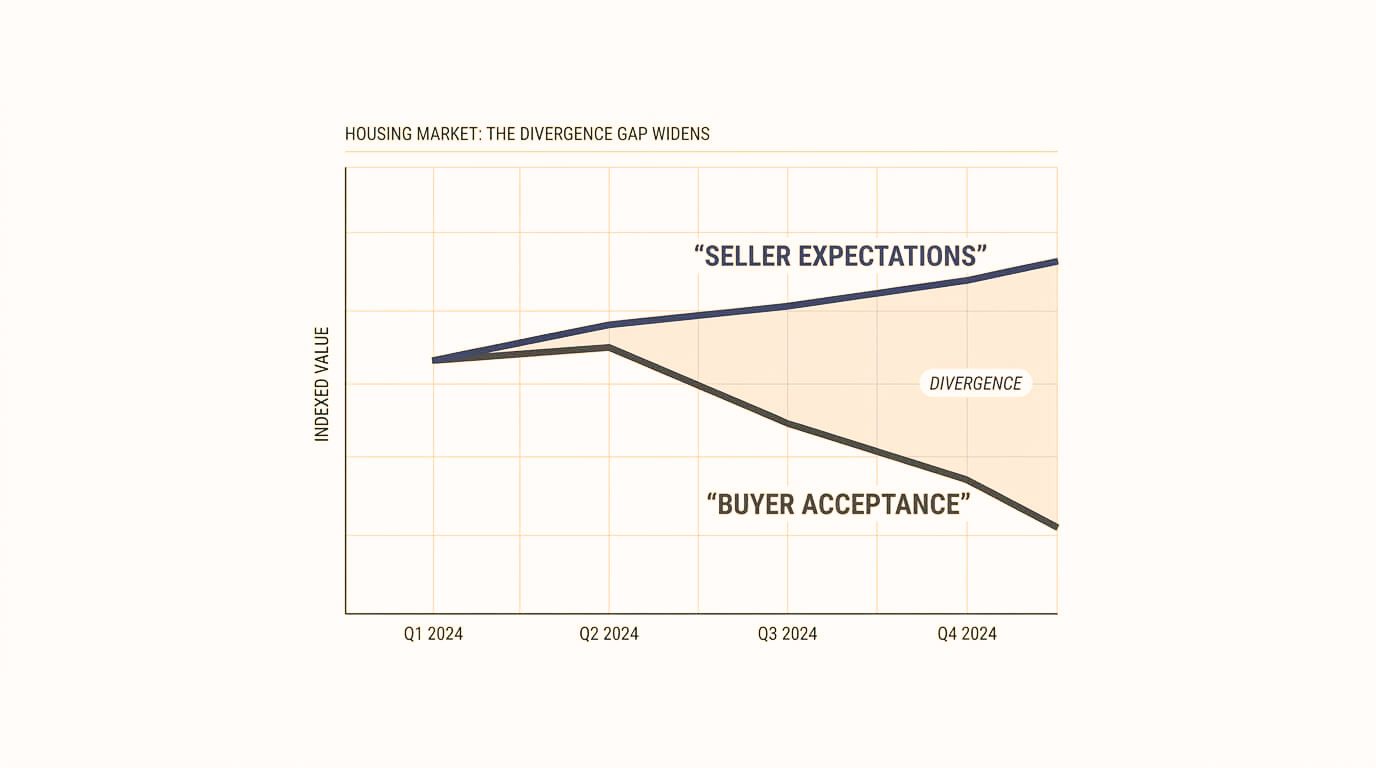

Roughly one-third of listings are cutting prices. Homes are selling—but only when priced right. Others are sitting. Deals are falling through. That’s not demand disappearing. That’s friction showing up.

We’ve said this before: affordability isn’t just about price—it’s about stability. When buyers hesitate, it’s not always because they can’t buy. It’s because the market feels uncertain.

HW’s data reinforces that view. Demand is still there. But it’s selective, cautious, and uneven.

Where we’d push further than HousingWire is this: the real risk isn’t pricing gaps—it’s execution gaps.

Builders don’t lose money because buyers negotiate. They lose when deals stall, financing shifts, or timelines stretch.

So yes—watch the spread between asking and accepted prices.

But more importantly, watch which builders can still move projects cleanly through that friction.

The winners aren’t the ones guessing direction. They’re the ones built to operate inside the uncertainty.

Read the full article here: What 10 years of housing data reveals about the 2026 market and the signals to watch