The Wall Street Journal just spotlighted a trend that’s reshaping the new-home market: big national builders offering ultra-cheap mortgages—sometimes as low as 0.99% in year one—to clear unsold inventory.

On the surface, these incentives look like a win for buyers. But the WSJ reporting shows a deeper problem: the cheap payment masks an inflated price.

Large builders achieve these rates through forward commitments—bulk-rate agreements that let them buy down mortgages without those incentives counting as seller concessions. Meaning: they can offer far richer perks than the rest of the market while keeping sticker prices high.

The result? Values get distorted.

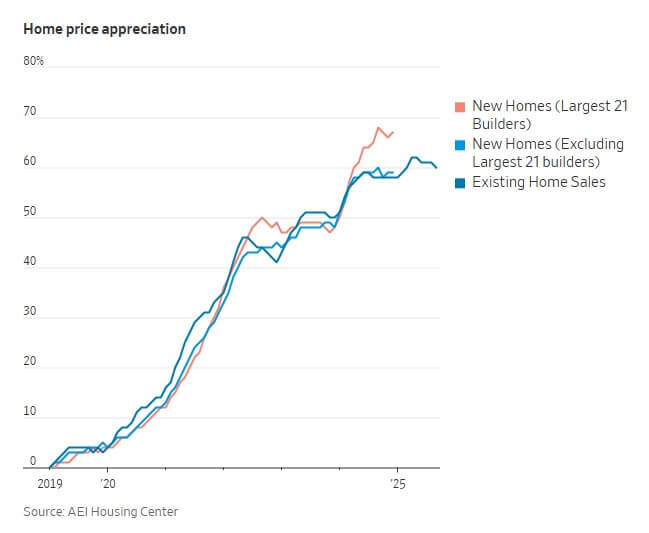

According to the WSJ, homes from the top 21 builders appreciated 6% more from 2019–2024 than comparable homes sold by smaller builders or resale sellers—not because they were worth more, but because buyers stretched further when given a discounted payment.

Now the bill is coming due.

- 27% of Lennar FHA borrowers (2022–24) are underwater.

- 18% of D.R. Horton FHA borrowers owe more than their home is worth.

Non-builder lenders show far healthier numbers.

This matters for every builder—not just the megas. Inflated comps eventually adjust downward, appraisals tighten, credit conditions react, and buyers lose trust when values sink faster than expected.

The takeaway is simple: cheap money can create expensive consequences. Sustainable financing protects the buyer, the market, and the builder long after closing day.